Apple has released its second-quarter earnings for fiscal 2025, showcasing a resilient performance amidst macroeconomic uncertainty, global supply chain shifts, and increased regulatory scrutiny. The tech giant beat Wall Street expectations, boosted by solid iPhone sales and record-setting growth in its high-margin Services division.

Financial Highlights at a Glance

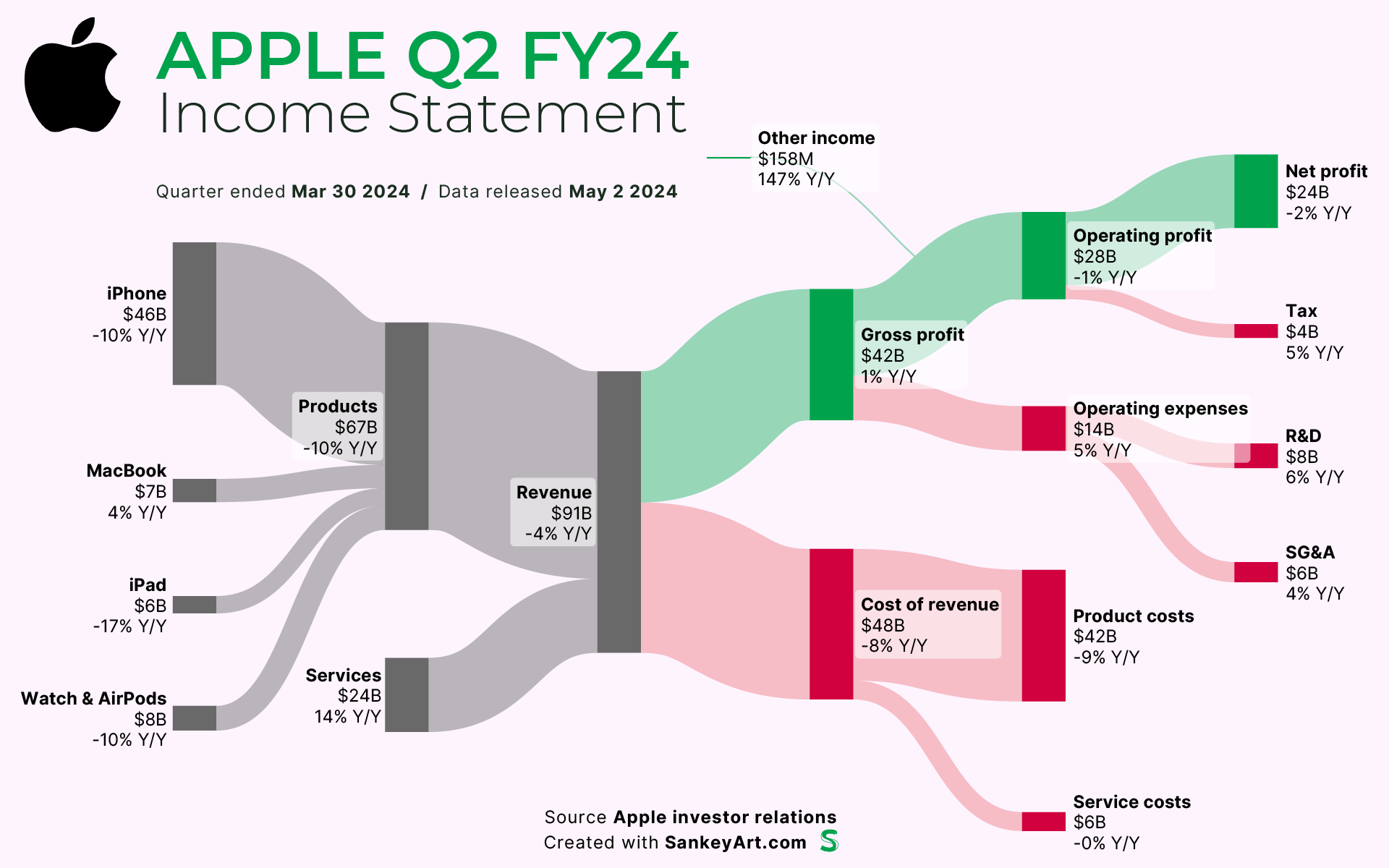

Total Revenue: $95.4 billion (Up 5% YoY, beating analyst expectations of $92.9B)

Earnings Per Share (EPS): $1.65 (Up 8% YoY, vs. expectations of $1.51)

Net Income: $24.78 billion (Driven by margin expansion in Services and improved supply chain efficiency)

Key Driver: The Services business, which includes iCloud, Apple Music, TV+, App Store, and AppleCare, continues to be a growth engine. Its 12% increase set a new record and helped Apple navigate hardware-related challenges.

iPhone: Despite global competition, iPhone sales remained robust, largely due to sustained demand for the iPhone 16 and the introduction of the mid-tier iPhone 16e in emerging markets.

Regional Performance & Global Strategy

Greater China Revenue: $16 billion (a 3% decline YoY) Attributed to intensified competition from domestic brands like Huawei and Xiaomi, alongside changing consumer sentiment.

Americas & Europe: Showed steady growth due to a mix of carrier promotions, educational partnerships, and new enterprise adoption for iPads and Macs.

Supply Chain Diversification in Motion

With rising geopolitical tension and increased U.S. tariffs on Chinese goods, Apple is accelerating its “China Plus One” strategy:

Vietnam is expanding its role in iPad and MacBook assembly, reinforcing Apple’s Asia-wide diversification.

Tim Cook confirmed that Apple is working with Foxconn and Pegatron to ramp up capacity in both countries, bolstered by local government incentives.

Tariffs and Regulatory Challenges

Apple disclosed it expects up to $900 million in additional costs next quarter due to newly introduced U.S. tariffs on Chinese-manufactured electronics. This comes as part of the broader U.S. trade policy overhaul under President Trump’s second administration.

While the company has absorbed most of these costs so far, Cook hinted that further geopolitical friction could eventually impact consumer prices or margins.

Artificial Intelligence: Siri Delays, Long-Term Focus

Despite the buzz surrounding AI in Big Tech, Apple admitted delays in its AI ambitions. Updates to Siri and other machine learning tools will likely roll out in early 2026.

However, the company stressed its commitment to on-device AI that preserves user privacy — a differentiator from rivals like Google and Meta who rely heavily on cloud processing.

Capital Allocation & Shareholder Updates

Dividend: Apple raised its quarterly dividend to $0.26 per share, a 4% increase.

Buybacks: The board authorized an additional $100 billion in stock repurchases, signalling confidence in long-term value creation.

Cash Reserves: Apple still maintains over $165 billion in cash and equivalents, keeping its balance sheet among the strongest in the industry.

Other Business Units

Other Bets (including Apple Car): While Apple has not disclosed a formal update on its automotive ventures, R&D spending rose 11% this quarter — largely linked to AI and autonomous initiatives.

Vision Pro: Early sales are “within internal expectations,” but no updated shipment numbers were provided.

Apple’s results show that while hardware growth is slowing, its pivot to services, digital ecosystems, and regional production diversification is helping the company navigate volatility better than many of its peers.

Its high-margin Services business and capital return program remain top draws for investors — even as the tech giant faces headwinds in China, regulatory threats, and delayed AI rollout.

Paul Balo is the founder of TechBooky and a highly skilled wireless communications professional with a strong background in cloud computing, offering extensive experience in designing, implementing, and managing wireless communication systems.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

{kind=link}