Nigeria’s Central Bank (CBN) has officially approved the launch of open banking, mandating that banks begin sharing customer data with other financial institutions starting by August 2025. This move makes Nigeria the first African country to implement open banking, arriving about four years after the CBN first released a regulatory framework for the initiative. Industry observers say the long-awaited rollout could fundamentally transform Nigeria’s banking and fintech landscape by unleashing innovation, boosting competition, and improving customer experience in financial services.

CBN Governor Olayemi Cardoso has emphasised the importance of open banking as a key part of Nigeria’s financial strategy for 2025. He noted that adopting an open banking framework will spur innovation in the fintech sector and improve financial service delivery and customer experience, aligning Nigeria with global trends.

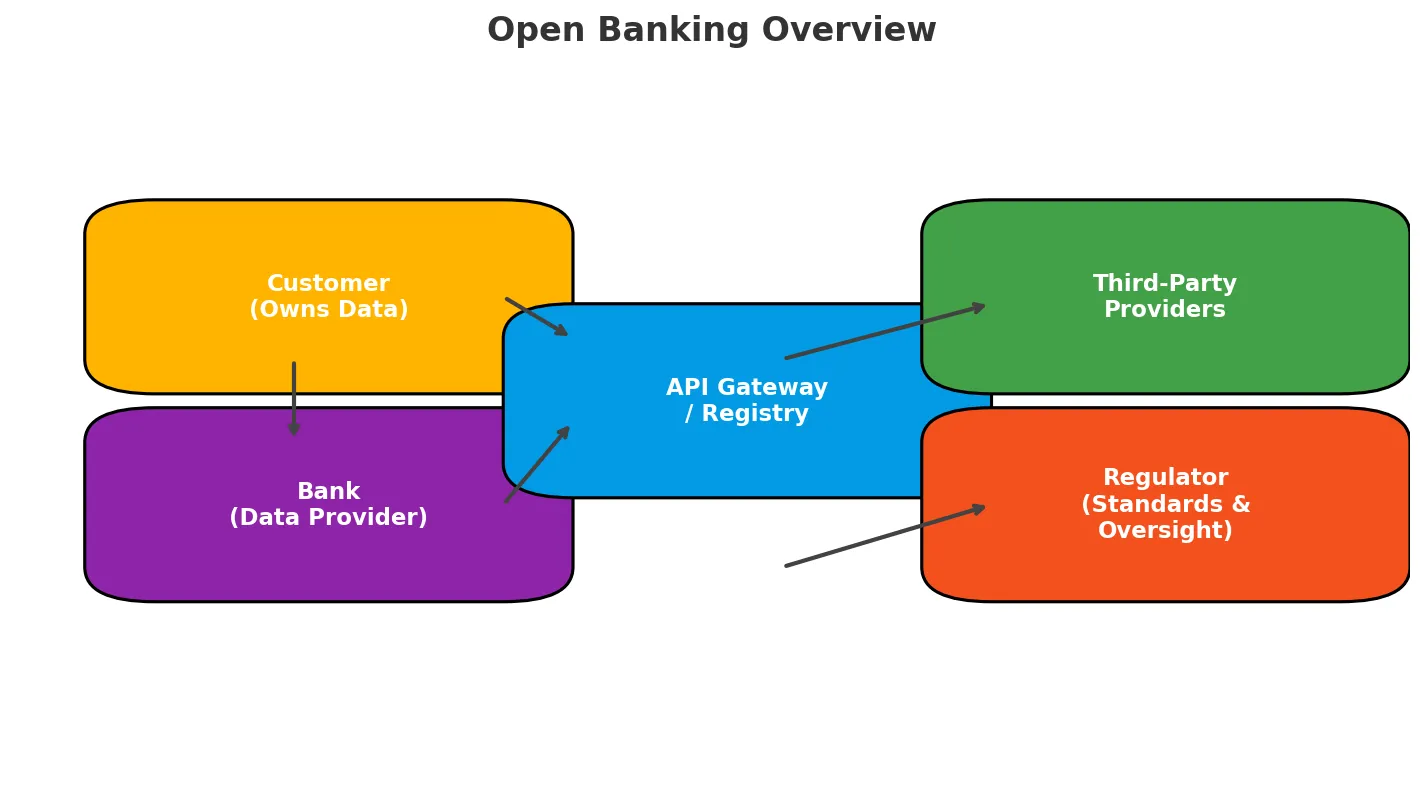

Open banking is a framework that allows banks and fintech companies to share financial data securely via standardised interfaces (APIs), but only with the customer’s consent. In practice, this means bank customers can decide to grant third-party providers (like fintech apps or other banks) access to their account information – such as balances, transaction history, and spending patterns – through secure APIs. The customer remains in control of who can see their data and for what purpose, essentially becoming “the gatekeeper of [their] own financial narrative”. This marks a significant shift from the traditional model where banks kept data siloed; previously, if you had accounts at multiple banks, each institution only saw a fragment of your financial picture. Open banking breaks down those walls, giving authorized service providers a more complete view (with your permission) and allowing new services like consolidated account dashboards, tailored budgeting tools, and smoother loan processes.

In Nigeria’s case, open banking has the potential to be a game-changer. As one columnist noted, this is “anything but ordinary” – it could “fundamentally change how Nigerians interact with their money”. For example, with open banking a customer applying for a loan could permit the lender to access their financial records across all their banks, not just one. This comprehensive data sharing could improve the customer’s credit profile, help them qualify for better rates, and eliminate tedious paperwork. Likewise, someone trying to budget or track spending could use a single fintech app to pull in data from all their accounts, giving a 360-degree view of their finances in one place. These are the kinds of convenient solutions that have already emerged in countries like the UK and Australia, where open banking has increased financial inclusion, spurred innovation, and empowered consumers to make more informed choices. Now, Nigeria is poised to reap similar benefits as it ushers in this new era of banking.

Nigeria’s road to open banking has been a long one, involving extensive planning and industry collaboration. The CBN first introduced the idea in 2019 and released a regulatory framework in 2021 to lay the groundwork. However, implementation did not happen overnight. There was initially some resistance from parts of the banking industry, especially over the CBN’s early plan to centralize the open banking system under the Nigerian Interbank Settlement System (NIBSS). Banks were concerned about ceding too much control to a single entity. In response to feedback from banks and fintech stakeholders, the CBN revised its approach – instead of running open banking through one central hub, it set up independent oversight committees composed of bankers and industry professionals to govern the system. These committees will oversee the integrity and security of the open banking ecosystem, with the CBN providing guidance but not micromanaging day-to-day operations. This compromise helped balance regulatory oversight with industry buy-in, fostering trust and collaboration needed to move forward.

The regulatory groundwork has steadily fallen into place. In March 2023, the CBN issued Operational Guidelines for Open Banking (the first in Africa) that spelled out how banks and other financial institutions should access and handle customer data securely. Now, with formal approval granted in April 2025, Nigeria is set to fully launch open banking by August. This timeline gives banks and fintech companies a few months to align their systems, form partnerships, and ensure compliance with the new standards before the system goes live. August 2025 may still seem far off, but the shift has already begun – banks, fintechs, and even asset managers are preparing to integrate their systems, and consumers should likewise get informed and ready to take advantage of the changes.

How Will Nigeria’s Open Banking Work?

When open banking goes live, it will operate under a well-defined framework to protect consumers and ensure smooth data sharing. Some key features of Nigeria’s open banking framework include:

Standardized APIs: All participating banks and fintech providers will connect through a uniform set of Application Programming Interfaces. This common standard ensures secure, seamless data exchange across the industry. In short, every institution “speaks the same language” technologically, which reduces integration friction.

Customer Consent Management: Access to any individual’s financial data will require that person’s explicit permission. Customers will manage their consents through a central system linked to their Bank Verification Number (BVN) – a unique ID every banked Nigerian has. This means you can authorize a fintech app to fetch your data, and you can just as easily revoke that access later. Privacy and control are built-in, as no data can be shared without the customer’s say-so.

Open Banking Registry: The CBN will maintain a secure registry of all accredited open banking participants (banks, fintechs, etc.). Every third-party service must be registered and authenticated. This registry acts as a safeguard against fraud: only verified, licensed companies can plug into the APIs to request data. Consumers can therefore trust that any app or service offering open banking features is vetted.

Data Security Standards: The guidelines enforce strict security and encryption standards for data sharing. Banks and fintechs must adhere to these protocols to protect customer information in transit and at rest. In essence, open banking in Nigeria is being implemented with a “security by design” approach. (Notably, industry proponents point out that open banking can actually enhance data privacy, since it replaces the old practice of some apps scraping your banking login or screen data with a far more secure token-based method.)

customers remain in full control of their data. They can decide which services to grant access, what specific data can be shared, and for how long. And if they change their mind, they can withdraw consent at any time, cutting off the data flow. This consumer-centric design is why open banking is often described as not just a technological leap but a mindset shift: it empowers the individual with the ability to securely share their financial information to get better services, rather than leaving that information locked up within one bank’s silo.

One of the biggest anticipated benefits of open banking in Nigeria is a burst of innovation and competition in the financial sector. By breaking down data barriers, open banking levels the playing field for fintech startups and smaller financial institutions to compete with established banks. They will be able to develop new apps and products leveraging banking data that was previously hard to access. According to Open Banking Nigeria (the industry-led coalition), “the financial ecosystem in Nigeria will accelerate as technical frictions are removed and innovation is unleashed.” In other words, open APIs mean fintech developers can more easily build services on top of banking infrastructure – akin to how innovators build smartphone apps on common platforms.

For consumers, this should translate into more choice and better offerings. When banks no longer have an exclusive hold on customer data, they must compete on service, pricing, and customer satisfaction – not just on locking in your funds. As The Nation newspaper notes, open banking “breaks down the walls between institutions and puts customers at the centre.” It’s a reform that creates room for better financial products, more transparent pricing, and ultimately a fairer ecosystem. We could see a wave of new Nigerian fintech services: from budgeting and expense tracking tools, to account aggregators that show all your finances in one view, to comparison apps that help you find the best banking products. Traditional banks, on their part, may partner with fintechs or develop their own improved digital offerings to keep up.

Importantly, Nigeria’s move aligns with global trends and could make its market more attractive for partnerships and investment. In the UK, which pioneered open banking in 2018, fintech innovation flourished – today over 10 million Britons and businesses use open banking-powered services, about 15% of the UK population, up from 6 million just 18 months prior. Across the EU, where open banking was mandated by the PSD2 regulation, the number of open banking users is forecast to reach about 63 million by 2024, a fourfold increase in four years. These millions of users have fuelled a vibrant fintech ecosystem in Europe. By launching its own open banking regime, Nigeria is signalling to fintech entrepreneurs and global investors that its financial sector is open for innovation on a comparable scale. The CBN itself has highlighted that Nigeria’s adoption of open banking is expected to “spur innovation and create new opportunities” in fintech, aligning the country with global financial technology trends.

Early indications suggest Nigeria’s fintech community is eager to seize the opportunity. For instance, local startups like Mono, Okra, and OnePipe have been building data-integration platforms for years in anticipation of open banking rules. With official APIs, their jobs get easier and more secure. We can expect a surge in collaborative products – e.g. bank-Fintech partnerships where a fintech uses banking data to offer specialized services (personal financial management, alternative credit scoring, etc.), or where banks integrate fintech services into their apps. “Open banking will unlock data, enabling banks to assess creditworthiness more efficiently. It will also drive traditional banks to innovate, as they will face competition from newer institutions better equipped to serve customers,”says Uzoma Dozie, a former bank Diamond Bank CEO turned fintech founder. In short, competition will increase, but so will opportunities for incumbents and challengers alike to innovate and differentiate themselves.

Enhancing Customer Experience and Financial Inclusion

From a customer perspective, open banking promises a more seamless and personalized banking experience. Nigerians today often juggle multiple bank accounts, mobile wallets, and finance apps without any integration – for example, you might use one bank’s app to check your salary account, another service to manage savings, and a separate lending app for loans, each requiring separate logins and lacking a holistic view. Open banking can simplify this. With your permission, an application could pull all that data together, giving you one dashboard for your entire financial life. This unified view can help you make more informed decisions – spotting where you spend the most, comparing rates between banks, or automating transfers and payments across accounts. Essentially, open banking turns the idea of “one customer, one bank” on its head; you become free to use any combination of financial services that suit you, and have them work in concert through data sharing.

Additionally, customers gain more power and control. If you’ve ever felt stuck with a bank because your history was there, those days are fading. With open banking, you can port your financial data to a new provider for a better offer. Want to switch banks or get a loan from a fintech? You can securely share your records instead of starting from scratch. This fosters a more competitive market for your business, meaning banks and fintechs must treat customers well or risk losing them. It’s telling that one of the core principles of Nigeria’s open banking framework is that customers “can revoke access at any time, maintaining full sovereignty over their financial data.” The customer is in the driver’s seat.

Crucially, open banking could also expand financial inclusion by enabling smarter lending and services for those who have been left out. Nigeria has an estimated 120 million banked customers, yet as many as 70% of those account holders do not have access to credit from formal lenders. This is largely because banks have traditionally been cautious, only lending to people with substantial collateral or credit histories. Millions of Nigerians – especially small business owners and individuals with informal incomes – struggle to get loans because banks don’t have enough data to assess their creditworthiness. Fintech lenders have tried to fill the gap, but with limited access to reliable banking data, they often resorted to using unconventional proxies (like mobile airtime or SMS records) and charging high interest to cover the risk. The result was a mix of subprime microloans and sometimes predatory collection practices.

Open banking changes the equation on credit. With customers’ consent, lenders can pull rich transaction histories and income data directly from bank accounts. This “more data means more trust, and more trust lowers the cost of lending,” as Uzoma Dozie explains. A fintech or bank assessing a loan application will be able to see salary deposits, bill payments, business revenues, and other cash flows that help paint a true picture of the applicant’s finances. Credit scoring becomes possible for millions who’ve never had a formal credit score. In fact, a key benefit touted is the creation of much-needed credit profiles for Nigerians using their actual bank data. With better data, lenders can extend credit to deserving borrowers previously deemed “thin file” or high risk, on more reasonable terms. This could unlock lending for many small and medium enterprises (SMEs) that drive the economy. “Many banks hesitate to lend to small businesses because they lack sufficient data on these enterprises, but open banking would allow smaller financial institutions to access this data and extend credit,” Dozie notes, highlighting the opportunity for SME finance.

Better data-driven lending should also lead to more responsible credit. When lenders can verify a customer’s income and expenses across accounts, they can tailor loan amounts and avoid over-lending. This helps reduce defaults and the need for harsh recovery methods. According to TechCabal’s report, open banking access will encourage lenders to move away from the recent “mixed bag of subprime loans and predatory collection methods” toward more sustainable credit models. All of this supports greater financial inclusion: more Nigerians, including those without collateral, can access loans and financial services that were out of reach before. In the long run, having a robust, shared data ecosystem can also enable new products for the unbanked – for instance, fintech apps might use open banking infrastructure plus telecom/mobile money data to onboard users who are not yet fully in the banking system.

Paul Balo is the founder of TechBooky and a highly skilled wireless communications professional with a strong background in cloud computing, offering extensive experience in designing, implementing, and managing wireless communication systems.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

{kind=link}