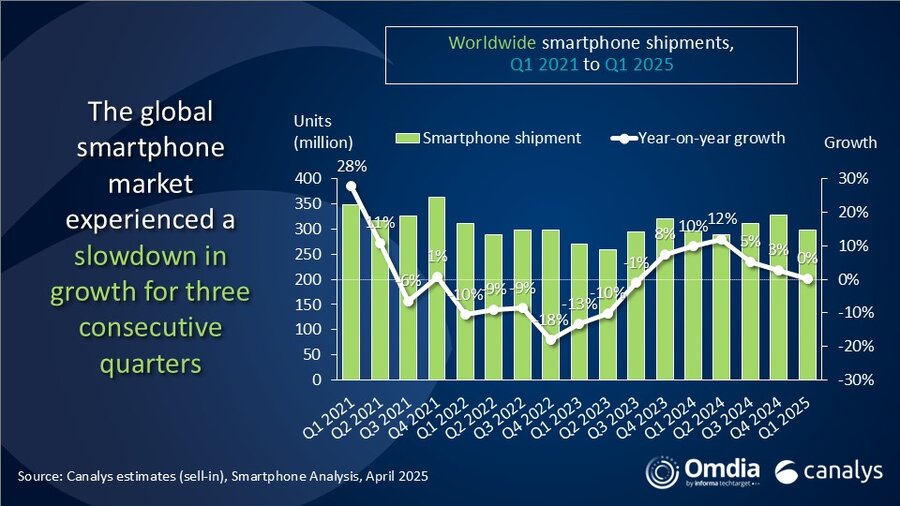

The global smartphone market experienced a slight year-over-year growth of 0.2% in Q1 2025, with total shipments reaching 296.9 million units, according to the latest research from Canalys (now part of Omdia). This marks the third consecutive quarter of slowed growth, attributed to the culmination of a peak replacement cycle and vendors’ focus on maintaining healthier inventory levels.

Top Global Smartphone Vendors

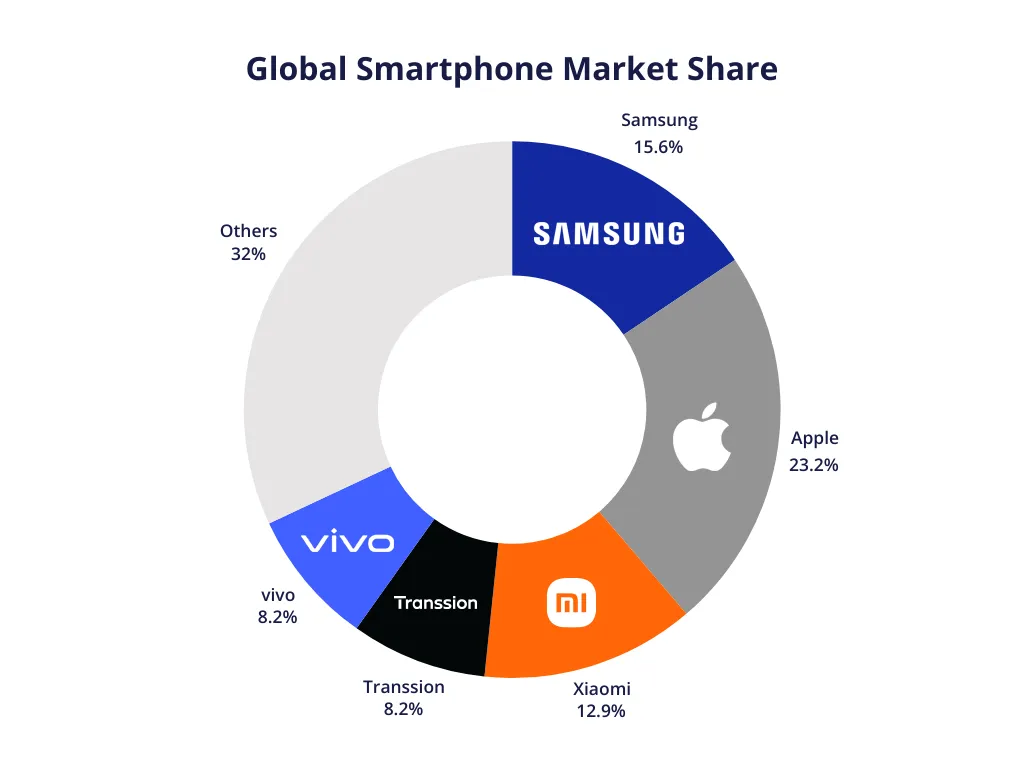

Samsung maintained its leadership position, shipping 60.5 million units and securing a 20% market share. This performance was bolstered by the launch of its latest flagship models and competitively priced new A-series products.

Apple followed closely, shipping 55.0 million units and capturing a 19% market share. Growth in emerging Asia Pacific markets and the United States contributed to Apple’s performance.

Xiaomi secured third place with 41.8 million units shipped, accounting for a 14% market share. The company’s diverse product ecosystem strengthened its brand in Mainland China and emerging overseas markets.

vivo and OPPO rounded out the top five, shipping 22.9 million and 22.7 million units, respectively, each holding an 8% market share.

Regional Market Dynamics

United States: The US smartphone market stood out with a 12% year-over-year growth in Q1, primarily driven by Apple’s proactive inventory build-up ahead of anticipated tariff policies. While iPhones produced in Mainland China still account for the majority of US shipments, production in India ramped up toward the end of the quarter, covering standard models of the iPhone 15 and 16 series, alongside accelerating production of the 16 Pro series.

Mainland China: Government subsidy programs stimulated growth, with Xiaomi returning to the top position for the first time in a decade by shipping 13.3 million units, a 40% year-over-year increase. Huawei followed closely with 13.0 million units shipped.

India: The market faced an 8% decline in shipments, totalling 32.4 million units, due to persistent demand weakness and elevated channel inventory from late 2024. vivo led the market with 7.0 million units shipped, capturing a 22% market share.

Europe: After a brief recovery, the European market experienced a decline, with vendors facing high flagship inventory from late last year and disruptions in mid- and low-end product lines due to the upcoming eco-design directive.

Africa: The region continued to benefit from vibrant retail activities and proactive market expansion efforts, demonstrating strong demand.

Despite the tepid performance in Q1, major smartphone brands have not adjusted their full-year shipment targets. They remain optimistic about a market rebound in Q2 and the second half of the year. Some regions, such as Southeast Asia and Latin America, already showed signs of gradual recovery in March. Additionally, decreasing inventory levels and the mid-year launch of new mid- and low-end products have boosted their confidence.

Related Reading

More contextual TechBooky stories selected from tags, categories and article context.

Paul Balo is the founder of TechBooky and a highly skilled wireless communications professional with a strong background in cloud computing, offering extensive experience in designing, implementing, and managing wireless communication systems.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

{kind=link}